How to Invest in an AIF in India

Introduction

Alternative Investment Funds (AIFs) have moved from a niche product for family offices to a mainstream allocation choice for Indian HNIs. Total commitments in the industry crossed ₹15.74 lakh crore by December 2025, and the number of registered AIFs has more than doubled in five years. If you are considering this route, the process is more structured than it looks.

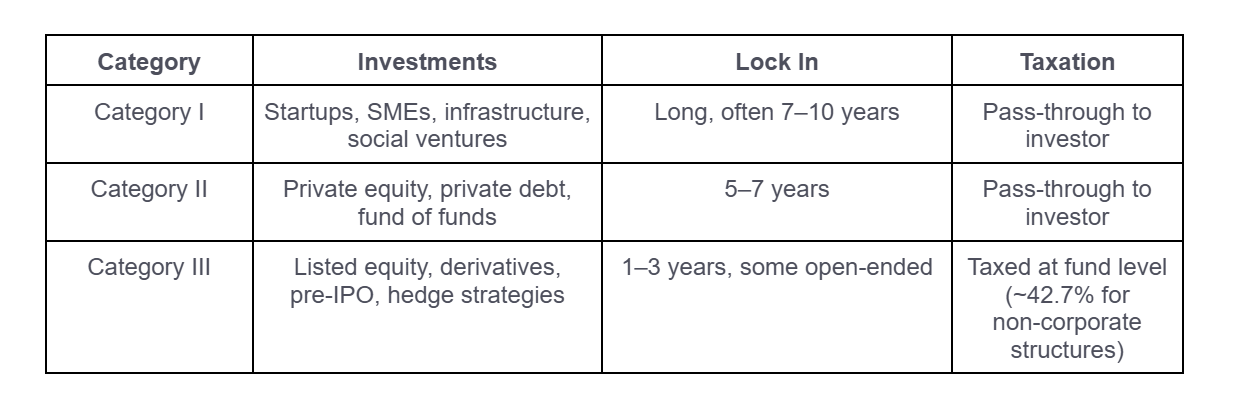

What is an AIF? An Alternative Investment Fund is a privately pooled investment vehicle registered with SEBI that raises capital from sophisticated investors and deploys it in unlisted equity, private credit, real estate, or listed markets through strategies mutual funds cannot use. AIFs are grouped into Category I, II, and III, each with its own risk profile, taxation, and investor eligibility. Entry requires a minimum commitment of ₹1 crore, and the fund is legally barred from soliciting the general public.

This guide walks through who can invest, how the categories differ, what documents are needed, and how to actually get from "interested" to "allotted." This roadmap guide covers the entire journey of investing in AIFs, including eligibility, category selection, the accreditation shift that changed the rules in 2025-26, documentation, the drawdown mechanism, and what to track once your capital is deployed.

From ₹1 Crore to Commitment: A Practical Guide to Investing in AIFs in India

Everything that happens between deciding to invest and actually being allotted units.

The ₹1 crore figure gets thrown around a lot when people talk about alternative investment funds, but very few explain what actually happens after you decide to write that cheque. India's AIF industry crossed ₹15.74 lakh crore in cumulative commitments by December 2025, up from ₹2.84 lakh crore just five years earlier. That growth has brought in a wave of new investors who understand the entry ticket but not the mechanics of getting from interest to allocation.

SEBI fixed the ₹1 crore minimum specifically to keep AIFs out of retail hands, reasoning that only investors with that level of capital have the balance sheet to absorb illiquidity and concentration risk. Fund employees, directors, and managers investing in their own scheme get a lower threshold of ₹25 lakh, since they are presumed to already understand the risk they're taking.

But ₹1 crore is only the regulatory floor. Large-value funds (LVFs) for accredited investors require a minimum ticket of ₹70 crore in exchange for lighter compliance obligations, and many fund houses set their own internal minimums above ₹1 crore depending on strategy and demand. Before assuming you qualify, check the specific scheme's PPM rather than relying on the regulatory baseline.

The Accreditation Shift That Changed the Onboarding Process

If you looked into AIFs a couple of years ago and are revisiting the idea now, the onboarding process has genuinely changed. SEBI notified the Third Amendment to the AIF Regulations in November 2025, formally creating a category of "Accredited Investor only" funds. These funds get real structural exemptions: the 1,000-investor cap doesn't apply to them, and their key investment team is exempt from NISM certification requirements.

Separately, a circular dated January 9, 2026, simplified how accreditation itself works. Previously, an investor needed a completed accreditation certificate before signing a contribution agreement, which slowed down final close timelines. Now, an AIF manager can execute the contribution agreement based on its own assessment of eligibility, though the capital still cannot be counted toward the fund's corpus until the accreditation certificate is formally issued. This is a meaningful operational relief for anyone trying to complete a commitment near a fund's closing date, but it doesn't remove the accreditation requirement; it only decouples the paperwork sequencing.

Getting accredited itself is a separate, one-time process through a SEBI-recognized accreditation agency, based on your net worth, income, or existing investment portfolio. As of the most recent data, the accredited investor base has grown more than 300% year-on-year, a sign that more fund houses are steering serious capital through this route.

Eligibility: Check If You Meet the Eligibility Bar

AIFs are not built for retail participation. The minimum investment for AIFs in India is ₹1 crore per investor, with a reduced threshold of ₹25 lakh for fund employees, directors, and fund managers investing in their own scheme. This ticket size is set by SEBI specifically to keep the product limited to financially sophisticated participants.

Eligible investors include:

Resident Indian individuals and HUFs

NRIs (subject to FEMA compliance)

Foreign nationals and institutional investors

Family offices, trusts, and corporates

Each scheme can accept a maximum of 1,000 investors, except angel funds, which are capped at 49. If you cannot commit ₹1 crore to a single scheme, an AIF is not accessible to you yet, and products like PMS or mutual funds remain the more realistic starting point.

Understand Which Category Fits Your Goal

Choosing the right AIF category is the single most important decision in this process, since it determines your liquidity, tax treatment, and risk exposure for the entire holding period.

Category I AIF funds carry government-linked incentives and back early-stage businesses, so returns are binary: a handful of successful bets often carry the entire portfolio. Category II AIFs, the largest segment by AUM, suit investors who want private market exposure without derivative risk. Category III AIFs are the only category permitted to use leverage and active trading strategies, which is why they attract investors coming from a PMS background who want similar flexibility with pooled-fund efficiency.

If capital preservation and shorter horizons matter more to you, Category III with its 1-3 year lock-in is usually the practical entry point. If you're comfortable being illiquid for a decade in exchange for outsized upside, Category I is worth exploring.

A regulatory update earlier this year also capped Category III leverage at 2x of net asset value, with fund managers now required to report leverage positions to SEBI daily. This tightened a previously looser framework and is worth asking about directly if you're evaluating a Category III scheme that markets aggressive strategies.

For Category II AIFs, SEBI has also reinforced the 10% concentration limit, meaning no single investee company can absorb more than a tenth of the fund's investable corpus without triggering additional disclosure and investor consent requirements. This rule exists precisely to prevent concentration risk from quietly building up in funds that investors assume are diversified.

Documentation: What Actually Gets Collected

Before you can commit capital, the AIF's registrar and transfer agent (RTA) will run standard KYC along with an accredited investor check, since some large-value schemes now require accreditation under SEBI's 2025 amendments. You'll need:

- PAN and Aadhaar

- Bank account details and cancelled cheque

- Net worth certificate (for accredited investor status, where applicable)

Once you've picked a category and fund, the operational checklist looks like this:

- PAN, Aadhaar, and standard KYC documents.

- Net worth certificate from a chartered accountant, if pursuing accredited investor status (SEBI no longer requires a detailed net-worth break-up in this certificate, only a confirmation that the threshold is met)

- FATCA/CRS declaration

- Demat account, since all AIF units have been mandatorily dematerialised since April 1, 2026, closing out the older system of physical unit certificates entirely

For NRIs, FEMA-compliant documentation and an NRE/NRO account routed for the specific investment

Reading the PPM Before You Commit

The Private Placement Memorandum is the only document that legally binds the fund to its stated strategy, fee structure, and risk disclosures. Because PPMs are not standardized across fund houses, two Category II funds can look similar in marketing material and differ substantially in their actual terms.

Three things are worth scrutinizing specifically: the fee structure (management fee plus a carried interest, usually 15-20% above a hurdle rate), the drawdown schedule, and the valuation methodology. On valuation, SEBI now requires independent portfolio valuation at least semi-annually for Category I and II funds, a tightening from the earlier annual requirement, so ask how recently the fund's holdings were last marked.

Commit Capital Through the Drawdown Model

Most AIFs, particularly Category I and II, follow a commitment-drawdown structure. You don't transfer the full ₹1 crore on day one. Instead, you sign a commitment for that amount, and the fund manager calls capital in tranches as investment opportunities arise. This reduces the "negative carry" of sitting on uninvested cash and is standard practice across the industry.

Category III AIFs, being closer to actively managed portfolios, more commonly ask for capital upfront or in one or two tranches rather than a long drawdown schedule.

Confirm which model applies before committing, since a fund calling capital faster than expected can create liquidity strain if you haven't planned for it.

Post-investment, SEBI mandates standardized reporting that didn't exist in this form a few years ago. Funds must now disclose performance against a relevant benchmark index in every investor communication, and NAV reporting follows a prescribed template designed to improve comparability across schemes. Related-party transactions and co-investment disclosures have also been tightened.

Practically, this means investors have more comparable data than before to judge whether a fund manager is delivering relative to peers and to the mandate laid out in the PPM, not just an absolute return number presented in isolation.

In Summary

Investing in an AIF in India requires a minimum commitment of ₹1 crore, KYC and investor classification, a careful review of the PPM, and comfort with a multi-year lock-in. The right category, whether Category I, II, or III, depends on your liquidity needs and risk appetite. AIFs suit investors who have already exhausted simpler avenues and want structured access to private markets.

Moving from a ₹1 crore commitment to actual allocation involves eligibility checks, category selection, PPM review, and a drawdown process that unfolds over years rather than days. Recent SEBI reforms, including the accreditation simplification and mandatory dematerialization, have made onboarding smoother, but the fundamentals of illiquidity, category-specific taxation, and manager due diligence remain unchanged.

0

17

0

Publish Date

02 Jul 2026

Reading Time

9 mins

Share On

Table Of Content

Introduction

From ₹1 Crore to Commitment: A Practical Guide to Investing in AIFs in India

The Accreditation Shift That Changed the Onboarding Process

Documentation: What Actually Gets Collected

Commit Capital Through the Drawdown Model

Tags

AIF

Alternative Investments Fund

AIF Investing in India

AIF Investments

Office Address: MiQB, Plot 23, Sector 18, Maruti Industrial Development Area, Gurugram, Haryana 122015

Registered Office Address: 1001, Block G1B, Pocket-1, Phase-2, Samriddhi Apartments, Dwarka Sector-18B, New Delhi-110078

Email: help@alphaamc.com • Phone: +91-93-1137-8001

Alpha Ventures Private Limited

(Formerly known as Planify WealthX Pvt Ltd)

Sponsor Name

Planify Venture LLP

Investment Manager

Fund Managers

VentureX Fund I (SME)

Other Websites

Disclaimer

You acknowledge and confirm that by accessing the website, you are seeking information relating to the organisation of your own accord and that there has been no form of solicitation, advertisement or inducement by the organisation. Any part of the content is not, and should not be construed as, an offer or solicitation to buy or sell any securities or make any investments or any products. No material/information provided on this website should be construed as investment advice. Any action on your part on the basis of the said content is at your own risk and responsibility.

Financial Documents

Policies

© 2026 Alpha AMC. All rights reserved, Built with ❤️ in India