The $50 Billion Middle Layer Nobody Talks About: India's API Industry is the Silent Engine of Global Pharma

Introduction

Every time someone swallows a pill, whether it's a generic paracetamol or a $10,000 cancer drug, a chain of decisions, chemistry, and capital stretches thousands of kilometres behind it. Most of that chain is invisible to the investor scanning balance sheets.

This series is about making that chain visible.

We chose pharma as our first industry because it has everything a serious investor needs to stress-test their mental models: deep science, regulatory complexity, global supply chains, pricing power questions, and Indian companies quietly dominating segments that global giants depend on.

This first piece is specifically about APIs (Active Pharmaceutical Ingredients). Not the pill you take. The molecule inside it that actually does the work.

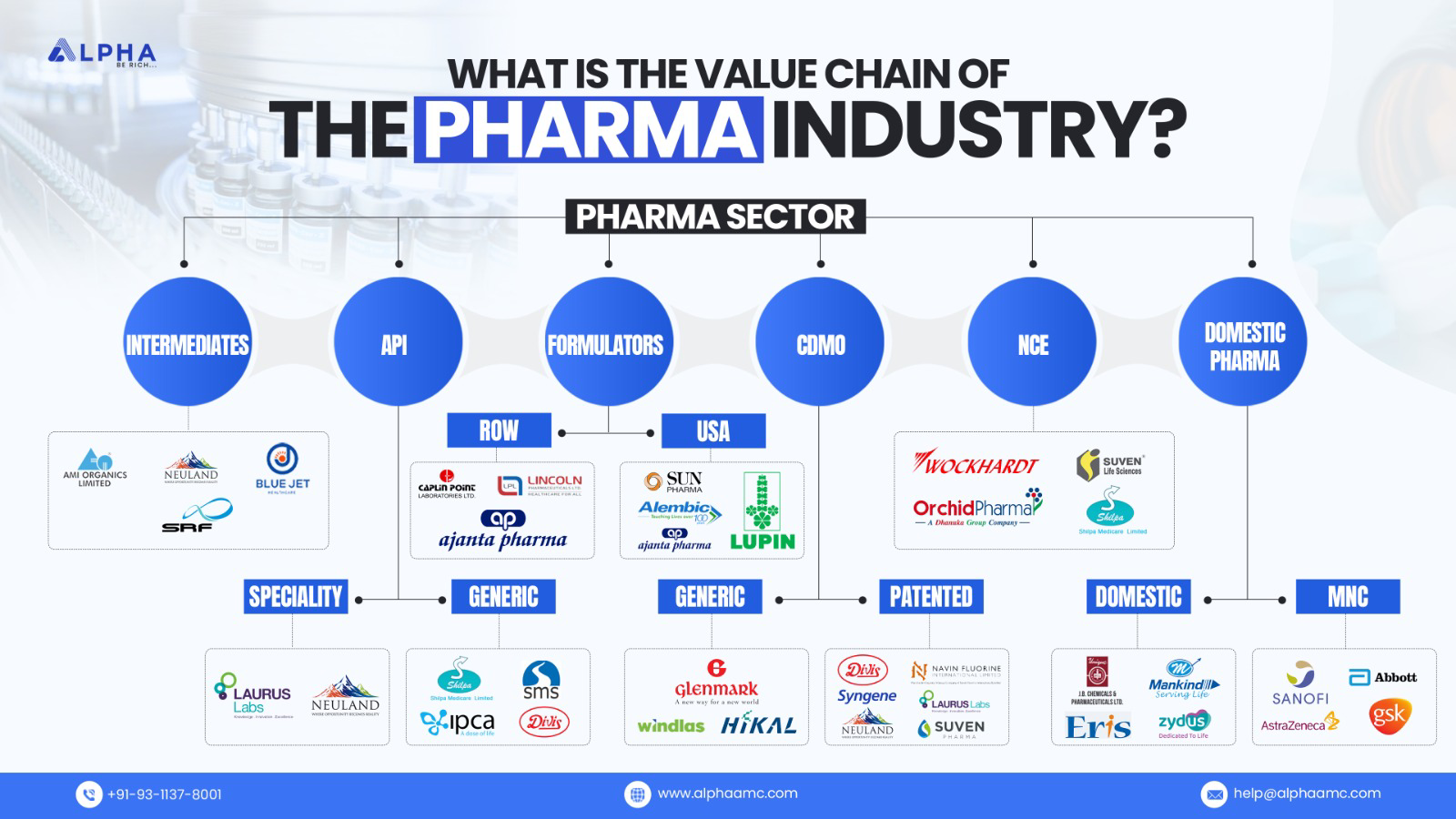

Where APIs Sit in the Chain?

1. Drug Discovery & Research (R&D) primarily includes the identification of disease targets as a first step, and takes it to the Molecule discovery/screening and then Pre-clinical testing. It is primarily characterised as

- Extremely high risk,

High reward but takes 10–15 years to commercialise

Very high failure rates

Primary players included in this section are: Innovators like Pfizer, Novartis

Margin Profile is: Potentially massive (blockbuster drugs), but highly unpredictable

Due diligence pointer: This is where IP is created, but not typical for Indian generic players.

2. Pharma Intermediates, otherwise known as KSM (Key Starting Material), the key raw materials to manufacture any medicine. In layman's language, imagine you're cooking a dish:

KSM → Raw ingredients (like flour, oil, spices)

Intermediates → Half-cooked steps

API → Final cooked dish (core drug)

Formulation → Plating/packaging (tablet/syrup)

They are the compounds used as building blocks in the multi-step synthesis of Active Pharmaceutical Ingredients (APIs). They are intermediate products formed during chemical processing that undergo further molecular changes or purification before becoming the final API. The margin profile ranges between 18% to 25%

Primary players include PI Industries, Ami Organics

Due Diligence pointers include, often better ROCE than APIs and Less regulatory burden.

3. API Manufacturing (Active Pharmaceutical Ingredients): It provides the pharmacological activity the "active" part that cures, treats, or prevents disease. They are characterised as high margin ones depending upon the kind of API (which we will discuss later in this handbook)

Players (India strong here): Divi's Laboratories, laurus Labs, Aarti Drugs etc.

4. Formulations (Finished Dosage): When a company converts API → tablets, injectables, syrups by mixing them with excipients and other preservatives, etc.

Types: Generics, Branded generics, & Speciality / complex generics

Primary Players included: Sun Pharmaceutical Industries, Dr. Reddy's Laboratories

Margins:

Highly variable:

India branded generics → high margin

US generics → price erosion

Due diligence pointer: Distribution + brand + regulatory approvals

5. Contract Development & Manufacturing (CDMO / CRAMS): Contract Development and Manufacturing Organisation is a company in the pharmaceutical industry that provides outsourced, integrated services for drug development and manufacturing. They assist pharma/biotech firms with everything from pre-formulation and clinical trial materials to large-scale commercial production.

Players: Windlas & Beta Drugs

6. Distribution & Marketing: It primarily includes selling drugs via doctors, Hospitals & Pharmacies

Types:

Branded generics (India)

Institutional sales

USFDA markets

Margins:

High in India (branding power)

Lower in regulated markets

What are the different types of API:

APIs can be classified:

By therapy (oncology, ARV, Hep-C, etc.)

By complexity (commodity → high-end)

By technology (synthetic, biologics, HPAPI)

(A) GENERIC APIs (commodity backbone) are Off-patent molecules and High-volume production. Examples: Paracetamol, Metformin. They are categorised as highly competitive & Price-driven

(B) ARV APIs (HIV drugs): APIs used for HIV/AIDS treatment. Examples: Tenofovir & Efavirenz. They are categorised as Large global programs (Africa, NGOs), the major consumption is in low-middle-income countries (LMIC) such as South Africa, Thailand, India, etc. They are Tender-driven and Dominated by Indian companies. Usually, an API constitutes ~25% to 35% of the cost of any formulation, whereas an ARV API constitutes ~75% of any formulation. The major funding for HIV is coming from two funds, the Global Fund and PEPFAR (1. A screenshot is attached for more details. The company needs multiple approvals to see these API’s. Maybe I will need them for a lifetime. hence dependency is more on these APIs.

(C) Hepatitis-C APIs (HEP-C): They are APIs for Hep-C antivirals. Examples: Sofosbuvir & Ledipasvir. Think: “bulk chemicals for pharma”. They are characterised as high-value, but finite lifecycle, & Demand peaked earlier. Competition is intense. Not much is regulated. The patient needs them for 12-14 weeks.

D) Oncology APIs (HPAPI): They are cancer drug APIs for chronic disease. and are characterized as HPAPI (High Potency APIs). Their main characteristics are extremely potent, low volume, high value and require containment. Example: Paclitaxel. They are high in margins but low in volume. Oncology API prices vary from $300/kg to $30,000/kg. More than 80% of the volumes are coming from imatinib & Gemcitabine. Prices for Imatinib are ~$350/kg and for Gemcitabine are ~$5000/kg. EBITDA margins are likely to be around 25%

E) Contrast Media API: Contrast media APIs are the active ingredients used to make contrast agents drugs injected into the body to improve visibility in medical imaging. When doctors do scans like a CT scan, MRI, X-ray, they inject a contrast agent so that Organs/, blood vessels/tumors become clearly visible

F) Speciality / Custom Synthesis APIs: They are APIs/intermediates made for innovator pharma; they are closest to CDMO. They are characterised as: Project-based, very sticky & high margin

G) Biologics / Peptides APIs: They are Large molecules made using biotech. Examples are insulin and monoclonal antibodies. They are characterised as extremely complex & very high entry barriers

We have compared all the API’s in different parameters that decide the growth journey of any API company:

Due diligence Pointer:

Commodity API → Volume game,

Specialty API → Margin + moat game &

CDMO → Relationship + visibility game

Revenue Mix of all API companies for better understanding, we will discuss this in detail in later chapters

Due Diligence Pointers:

Low-end API → commodity → price competition

Mid-tier API → therapy-driven → cyclical

High-end API → specialty → moat

CDMO → relationship → premium valuation

Not all APIs are equal — the real money is in complex, niche, and relationship-driven API.

Distribution Channel of various parts of Pharma :

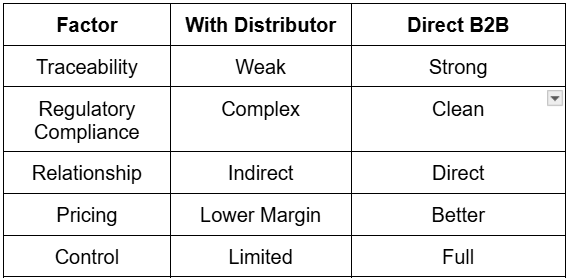

Why APIs Don't Use Distributors

API: Unlike branded pharma, API companies are pure B2B businesses. They don’t sell to patients, doctors, or chemists. They sell to other pharma companies

1. Primary distribution channel (core): B2B direct sales to pharma companies. The Buyers are: Branded generic companies, CDMO players, Innovator pharma

2. Export distribution: Direct exports to global pharma companies

US, EU, LATAM, MENA markets

Requires: U.S. Food and Drug Administration approvals & DMF filings

But to reach the export market, what distribution channel does an API follow:

Route 1: Regulatory filings (MOST IMPORTANT)

✔ DMF (Drug Master File)

Filed with regulators like U.S. Food and Drug Administration

What happens:

API company files DMF - Global pharma companies search for approved suppliers - They shortlist vendors. This is the entry ticket into global markets. Now the question is what DMF is and how anyone can check a supplier of API.

Below is the link for DMF Site:

https://www.fda.gov/drugs/drug-master-files-dmfs/list-drug-master-files-dmfs

Route 2: Direct business development

API companies actively: Approach:

Generic pharma companies

CDMOs

Through: Sales teams & Industry contacts

Route 3: Pharma exhibitions & platforms

Example: CPhI Worldwide & Bio International

Here: API companies meet global buyers & build relationships

It’s purely a B2B supply & distribution channel.

3. CDMO / contract manufacturing channel

Long-term supply agreements: API company ↔ CDMO / innovator pharma

Multi-year contracts

Volume commitment

Very sticky + high visibility

4. Trader/merchant exporters (small share)

- Commodity APIs

Smaller orders

This route is characterised as having lower margins & Less preferred by quality players.

Channel Mix for API Company

Due diligence pointers: The pointer, while analysing an API company, is the distribution channel, and exports have better margins, but with geographical and current risks. The real moat in API exports is not distribution, it is regulatory approval + customer stickiness

Now a question arises: Why don’t APIs use distributors?

Answer: APIs don’t use distributors because the “customer” is a regulated manufacturer, not a consumer. So trust, traceability, and compliance matter more than reach.

1. APIs are not products; they are critical inputs. APIs go directly into drug manufacturing

Any issue → entire batch failure/patient risk

So buyers (pharma companies) want full control over the supplier, Not an intermediary

2. Regulatory compliance requires direct traceability: To sell APIs globally, companies must comply with regulators

Requirement:

Full traceability of source

Batch-level documentation

Audit trail

If a distributor is involved, then the chain becomes complex, and accountability becomes unclear

3. Customer approval is manufacturer-specific (Most Important)

Before buying a pharma company: Audits the API plant, Validates processes, Links product to: DMF (Drug Master File)

API manufacturer-specific, not product-generic

Let’s compare the distribution channel of all listed API companies

Why this matters (investor lens): Divi’s model

Commodity API players (Aarti Drugs type)

Distribution = transactional

Many buyers

Low switching cost

Scaled API players (Laurus / Granules)

Distribution = mixed

Some stickiness

Better margins

High-end API/CDMO players (Divi’s / Neuland)

Distribution = relationship moat

Few clients

Deep integration

Final Takeaway

Question: Why are we saying that Lauraus has more depth in his channel as compared to Divi's, when they both are supplying direct

Answer: Both Laurus Labs Ltd and Divi's Laboratories Ltd supply directly (B2B), so at a surface level, their “distribution channels” look identical.

The difference is not in the channel type (both are direct)

The difference is in channel depth = how far they extend into the customer’s value chain. It is how many layers of the pharma value chain you participate in for your customer

1. Divi’s: Deep but focused (API + custom synthesis): Where Divi’s plays:

APIs

Intermediates

Custom synthesis (CRAMS-like)

Customer interaction: Divi’s → Innovator / Generic pharma

Very strong in: Scale, cost efficiency, long-term supply.

Insight: Divi’s goes deep within the API layer, but doesn’t extend beyond it

2. Laurus: Broader + deeper (API + CDMO + formulations): Where Laurus plays:

APIs

CDMO (contract manufacturing)

Finished dosage (formulations)

Customer interaction: Laurus → API → CDMO → Finished drug → Patient markets

The same client can: Source API, Outsource manufacturing, Use Laurus for formulations

Insight: Laurus is embedded across multiple layers of the same customer’s value chain.

Why this matters (investor lens): Divi’s model

- Strength: High efficiency & large-scale manufacturing

Risk: Limited participation beyond API

Laurus model

Strength: More wallet share per customer, multiple revenue levers

Risk: More complex execution

Both companies Use direct B2B distribution; however:

Divi’s depth = within the API layer

Laurus depth = across API + CDMO + formulations

Due diligence pointers: Divi’s sells deeply into one layer, Laurus sells across multiple layers of the same customer

Enough of the distribution channel but how would an investor understand that which model (Divi’s vs Laurus) creates better long-term returns

Divi's Laboratories Ltd model: (API + Custom synthesis / CRAMS-like leads very high ROCE, Asset-light relative to scale, Long-term innovator relationships & Limited competition in custom synthesis.Historically: More consistent, compounding returns

Laurus Labs Ltd model: API + CDMO + Formulations which leads to higher growth optionality, Multiple revenue streams, Ability to move up the value chain

Challenges: More capital-intensive, More execution complexity, Cyclicality (ARV, CDMO ramp-up)

Today, the market is clearly rewarding CDMO / CRAMS / complex chemistry models more than pure API models

But with a nuance:

High-quality API + custom synthesis (Divi’s) → still premium

Commodity API → discounted

CDMO / platform models (Laurus-type) → rewarded for future growth

So what do the above pointers tell an analyst to see while evaluating 2 players:

CDMO is structurally faster-growing

India CDMO market growing ~13%+ CAGR vs API ~7–8%

Global pharma outsourcing is increasing (China+1, cost pressure)

Translation: More outsourcing → more CDMO demand → higher valuations

CDMO margins are structurally higher: CDMO gross margins are ~25% higher than generic API. Hence, the market always pays for: Higher margin & higher visibility Market behaviour Laurus P/E expanded significantly (growth re-rating), whereas Divi’s remains premium but stable, which can be witness of last 3 years return profile. Hence, in short words - Growth optionality → re-rating & Stability → steady premium

What model market is rewarding

Answer: Tier 1 (Most rewarded today): CDMO / CRAMS / complex chemistry

Examples:

Laurus Labs Ltd (CDMO pivot)

Syngene International Ltd

Why: Outsourcing boom, High margins & long-term contracts

Tier 2 (Still premium) : High-quality API + custom synthesis

Example: Divi's Laboratories Ltd

Why: Proven execution, strong ROCE & sticky innovator clients

Tier 3 (Not rewarded much): Commodity API players

Example: Aarti Drugs, etc.

Why: Price competition & no differentiation

3. Why the market prefers CDMO Today:

- Structural outsourcing trend & Big pharma: Cutting costs & Outsourcing manufacturing. India is benefiting from China+1

- More complex molecules: Shift toward:

- HPAPI

biologics

peptides

Requires: CDMO capabilities

Reason 3: Visibility + stickiness CDMO contracts: Multi-year & high switching cost

Predictable cash flows → higher valuation

More complex molecules: Shift toward:

That’s why: Laurus-type stories get re-rated, but Divi’s stays premium, but doesn’t explode

Final Words

Today’s market is rewarding:

CDMO / CRAMS/platform models (highest)

High-quality API + custom synthesis (next best)

Commodity API (least rewarded)

One-line takeaway: The market is shifting from “who makes APIs cheapest” to “who can solve complex pharma problems”

To be Continued: Let’s stay in touch to understand what a small company needs to become the next Divi’s and Lauras!

0

79

0

Author

Diksha Kalra

Publish Date

21 Apr 2026

Reading Time

13 mins

Share On

Table Of Content

Introduction

What are the different types of API:

Distribution Channel of various parts of Pharma :

Let’s compare the distribution channel of all listed API companies

Final Takeaway

Tags

Office Address: MiQB, Plot 23, Sector 18, Maruti Industrial Development Area, Gurugram, Haryana 122015

Registered Office Address: 1001, Block G1B, Pocket-1, Phase-2, Samriddhi Apartments, Dwarka Sector-18B, New Delhi-110078

Email: help@alphaamc.com • Phone: +91-93-1137-8001

Alpha Ventures Private Limited

(Formerly known as Planify WealthX Pvt Ltd)

Sponsor Name

Planify Venture LLP

Investment Manager

Fund Managers

VentureX Fund I (SME)

Other Websites

Disclaimer

You acknowledge and confirm that by accessing the website, you are seeking information relating to the organisation of your own accord and that there has been no form of solicitation, advertisement or inducement by the organisation. Any part of the content is not, and should not be construed as, an offer or solicitation to buy or sell any securities or make any investments or any products. No material/information provided on this website should be construed as investment advice. Any action on your part on the basis of the said content is at your own risk and responsibility.

Financial Documents

Policies

© 2026 Alpha AMC. All rights reserved, Built with ❤️ in India